Insuring the Irreplaceable: Policy Structuring for Rare Crystal Collections

Rare crystal collections are usually insured well only when the policy is built around evidence, not sentiment. The practical structure is: document what each important piece is, establish a credible valuation basis, decide which pieces need scheduled coverage or a valuable-property floater/endorsement, then confirm the limits, exclusions, deductibles, storage rules, and claim documentation in the actual policy.

That is the core of gemstone collection insurance. A collection can be personally irreplaceable, but reimbursement depends on what the insurer has agreed to cover and what records exist before a loss.

broader context

Citrine verification note

This narrower page works best after the broader citrine reference page.

Start with item identity, not just rarity

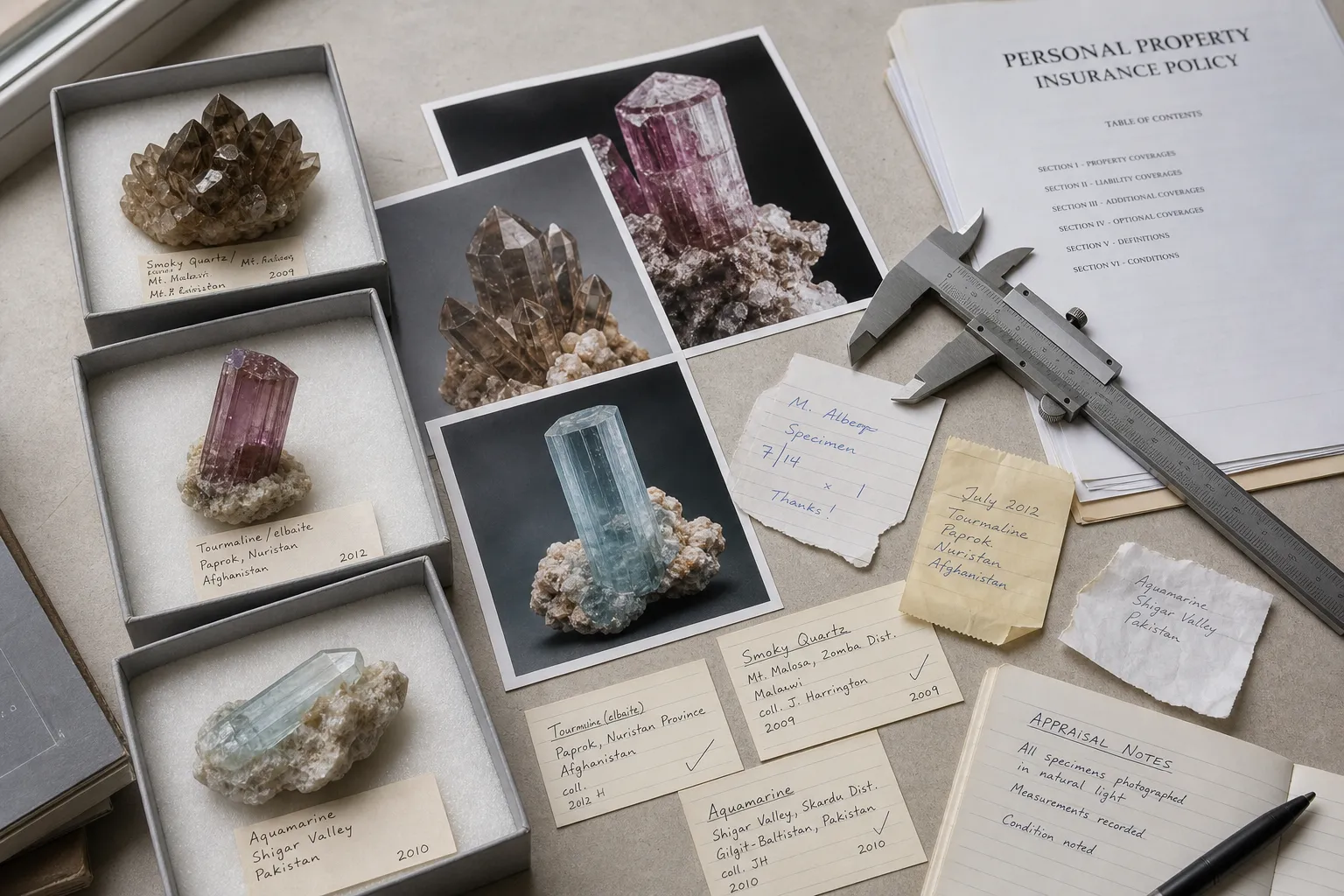

Collectors often describe a specimen in meaningful language: a locality citrine point, an untreated quartz cluster, a piece from an old collection, or the one object they would never sell. That language may be true and important, but insurance usually needs a more practical trail.

Identity records may include

- Clear photographs from several angles.

- Dimensions, weight, and visible identifying features.

- Purchase receipts or bills of sale.

- Inventory numbers or catalog entries.

- Provenance notes, including prior ownership or stated locality.

- Gemological reports where identity or treatment matters.

- Treatment disclosures when known.

- Storage and custody notes for higher-value pieces.

The first common misunderstanding is simple: a beautiful description is not the same as an insurable identity record. If a stone is stolen, damaged, lost, or disputed, the process is likely to focus on whether the item can be matched to a documented object.

For faceted gems, mounted stones, unusually valuable specimens, or items with disputed identity, a gemological report can help answer, “What is this?” But it is not the same as an appraisal for insurance. An appraisal addresses a value opinion for a stated purpose. A policy schedule answers a separate question: “What has the insurer accepted for coverage, and under what terms?”

Those three records can support each other, but they should not be treated as interchangeable.

Appraised value, purchase price, and collector value are different

A rare crystal insurance appraisal should do more than repeat a seller’s label. A stronger report explains the item, the valuation purpose, the relevant market, assumptions, limiting conditions, and valuation date. Professional appraisal standards can help make valuation work more disciplined, but the exact appraisal requirements depend on the insurer, policy form, assignment, and jurisdiction.

How common records differ

Purchase receipt

Can support what you paid and when. It does not automatically prove current insurable value.

Seller description

Can support how the item was marketed. It does not automatically prove independent identity or value.

Gemological report

Can support material identity and observed features. It does not automatically prove insurance replacement value.

Provenance notes

Can support ownership history or locality context. They do not automatically prove reimbursement amount.

Insurance appraisal

Can support a value opinion for a stated purpose. It does not automatically prove claim approval.

Policy schedule

Can support items and limits accepted by the insurer. It does not automatically create coverage beyond policy terms.

Purchase price may matter, especially for recent acquisitions. But appraised value versus purchase price can diverge when the market changes, the seller’s description is incomplete, the item was bought below or above market, or the appraisal uses a different value premise. Retail replacement value, auction value, wholesale value, estate value, and a collector’s personal value are not the same thing.

Emotional value also sits outside the usual insurance calculation. A crystal can mark a life event, a locality connection, a practice, or years of searching. Insurance generally works through documented financial value and covered loss terms. That does not reduce the meaning of the object; it only defines the evidence system a claim is likely to enter.

Why homeowners coverage may not be enough

Homeowners coverage for crystals can help, but it should not be assumed to cover a serious collection in full. Ordinary personal property coverage may include limits, sublimits, deductibles, exclusions, and documentation requirements. Valuable items may need separate attention through scheduled personal property, a floater, or an endorsement.

Insurance education sources commonly describe floaters and endorsements as ways to add or modify coverage for valuable personal property. That mechanism can be relevant to gems and crystals, but it does not mean every policy treats every mineral specimen the same way. A loose faceted gem, a mounted stone, a mineral cabinet, a museum-quality specimen, a dealer’s inventory, and a personal crystal collection may fall into different categories.

Before relying on a policy, ask practical questions

- Are the most valuable pieces named or scheduled?

- Are lower-value pieces covered under a blanket limit, and is that limit enough?

- Are theft, fire, water damage, accidental breakage, transit, or mysterious disappearance addressed?

- Does a deductible apply, and does it differ for scheduled items?

- Are there exclusions for fragile items, gradual deterioration, shipping, display, business use, or off-premises storage?

- Does the insurer require photos, receipts, appraisals, lab reports, safe storage, or updated records?

- Is settlement based on agreed value, replacement cost, actual cash value, or another method?

- What documentation would be needed at claim time?

These are policy-language questions. Confirm them in writing with the insurer, agent, broker, or another licensed insurance professional. In the United States, insurance is state-regulated, so state insurance department resources may also matter.

A practical way to structure coverage

For most collectors, the cleanest structure is not the most complicated one. It is the one that matches the collection’s risk and evidence.

1. Individually significant pieces

These are pieces whose loss would be financially meaningful on their own: an exceptional mineral specimen, a high-value natural citrine, a rare locality crystal, a notable untreated stone, a large faceted gem, or an item with strong provenance. These are the first candidates for scheduled coverage or item-level review.

For each one, keep photographs, dimensions, purchase records, provenance notes, lab reports if relevant, and appraisal documentation if the insurer requires or accepts it.

2. Mid-value pieces that matter as a group

Many collections are built from dozens or hundreds of specimens that are not all individually expensive, but together represent substantial value. Blanket personal property coverage may not be enough if the total value exceeds ordinary limits or if valuable-property restrictions apply.

For this group, a consistent inventory is more useful than a perfect museum catalog. Another person should be able to understand what exists, where it came from, and how values were estimated.

3. Low-value or study pieces

Not every crystal needs a formal appraisal. Some items may be adequately documented with photographs, receipts, and an inventory. The goal is not to over-document inexpensive pieces; it is to avoid leaving valuable or hard-to-identify items unsupported.

This grouping prevents two opposite mistakes: assuming every small specimen needs formal valuation, or assuming a cabinet full of modest pieces has no insurance significance as a collection.

The policy terms decide what reimbursement can look like

Gemstone insurance policy limits are not just headline dollar amounts. They are shaped by definitions, covered causes of loss, exclusions, deductibles, schedules, location rules, and documentation conditions.

A policy may not use collector-friendly words like “rare crystal cabinet” or “citrine cluster.” It may classify property as jewelry, valuable articles, collectibles, personal property, business property, fragile items, or another category. That classification can affect both coverage and settlement.

Useful questions include

- Is the item treated as jewelry, a mineral specimen, a collectible, or general personal property?

- Are loose stones covered differently from mounted stones?

- Are display pieces covered if they are not worn as jewelry?

- Are pieces covered at a gem show, appraiser’s office, storage unit, shipping carrier, or temporary residence?

- Is accidental breakage covered, or only named events such as theft or fire?

- Are there security expectations for high-value scheduled items?

- Does the insurer require updated appraisals after a certain period?

- If a piece is one-of-a-kind, how is value determined?

Public sources can support these as cautious planning questions, not universal answers. Exact limits, exclusions, appraisal intervals, deductibles, settlement methods, and storage requirements have to come from the policy and the insurer’s written guidance.

Build the records before anything goes wrong

Insurance documentation for crystals is strongest while the collection is intact. After a loss, reconstructing ownership, identity, and value from memory, old emails, vendor labels, or partial photos is much harder.

A useful records file may include

- A master inventory with item numbers.

- Dated photographs.

- Receipts and invoices.

- Appraisal reports.

- Gemological reports.

- Correspondence about provenance or treatment.

- Storage records.

- Insurance schedules and declarations.

- Notes on items sold, gifted, recut, repaired, or reclassified.

Be careful with provenance language. “Purchased as Brazilian citrine from Seller X in 2024” is different from “confirmed Brazilian natural citrine.” Locality, treatment status, and natural-versus-treated identity can affect value, but they should be stated according to the strength of the evidence. A collector’s memory, a vendor card, and a laboratory report do not carry the same weight.

Advanced gemology can help characterize valuable or disputed stones in specialized settings, but that does not mean advanced scanning or database registration is normally required for insurance. For most collectors, the more important step is having clear, consistent, insurer-usable documentation.

Common confusion to avoid

“Rare” does not automatically mean scheduled.

Rarity may support value, but the insurer still needs documentation and an accepted coverage structure.

“Appraised” does not mean covered.

An appraisal can support valuation. The policy decides coverage.

“Covered under homeowners” does not mean covered enough.

Blanket personal property coverage may have limits or exclusions that matter for a valuable collection.

“I have a lab report” does not mean “I have an insurance value.”

A lab report helps with identity. It does not replace an appraisal or a policy schedule.

“Irreplaceable” does not mean the insurer can recreate the object.

Insurance may compensate according to policy terms, but it cannot restore personal history, provenance, or meaning.

The clean next step

Before asking for coverage, prepare a short packet: inventory, photographs, purchase records, lab reports, appraisals, and a list of the pieces you believe need item-level treatment. Then ask the insurer or licensed professional which items should be scheduled, whether a floater or endorsement is available, what documentation is required, and which limits or exclusions would apply.

That is the practical heart of protecting hard assets in a crystal collection: connect the object, the evidence, the valuation, and the policy language before a loss, rather than assuming ordinary coverage or personal meaning will carry the claim.